HELOC vs Home Equity Loan: Which Is Right for You?

BRIAN SIDE

BRIAN SIDE

One of the most common conversations I have with homeowners today starts with a simple question:

"I have equity in my home. What's the smartest way to use it?"

Whether you're considering a major renovation, building an ADU, consolidating debt, funding a business opportunity, or purchasing an investment property, the answer isn't always straightforward.

Two options typically rise to the top:

Home Equity Line of Credit (HELOC)

Home Equity Loan (HELOAN)

Both allow homeowners to borrow against the equity they've built. Both use the home as collateral. Yet they work very differently, and choosing the wrong option could cost thousands of dollars over time.

As a real estate advisor, I've helped many homeowners evaluate these decisions alongside trusted lending professionals. While I'm not a mortgage lender, understanding how these tools work can help you have a much more productive conversation when it's time to explore your options.

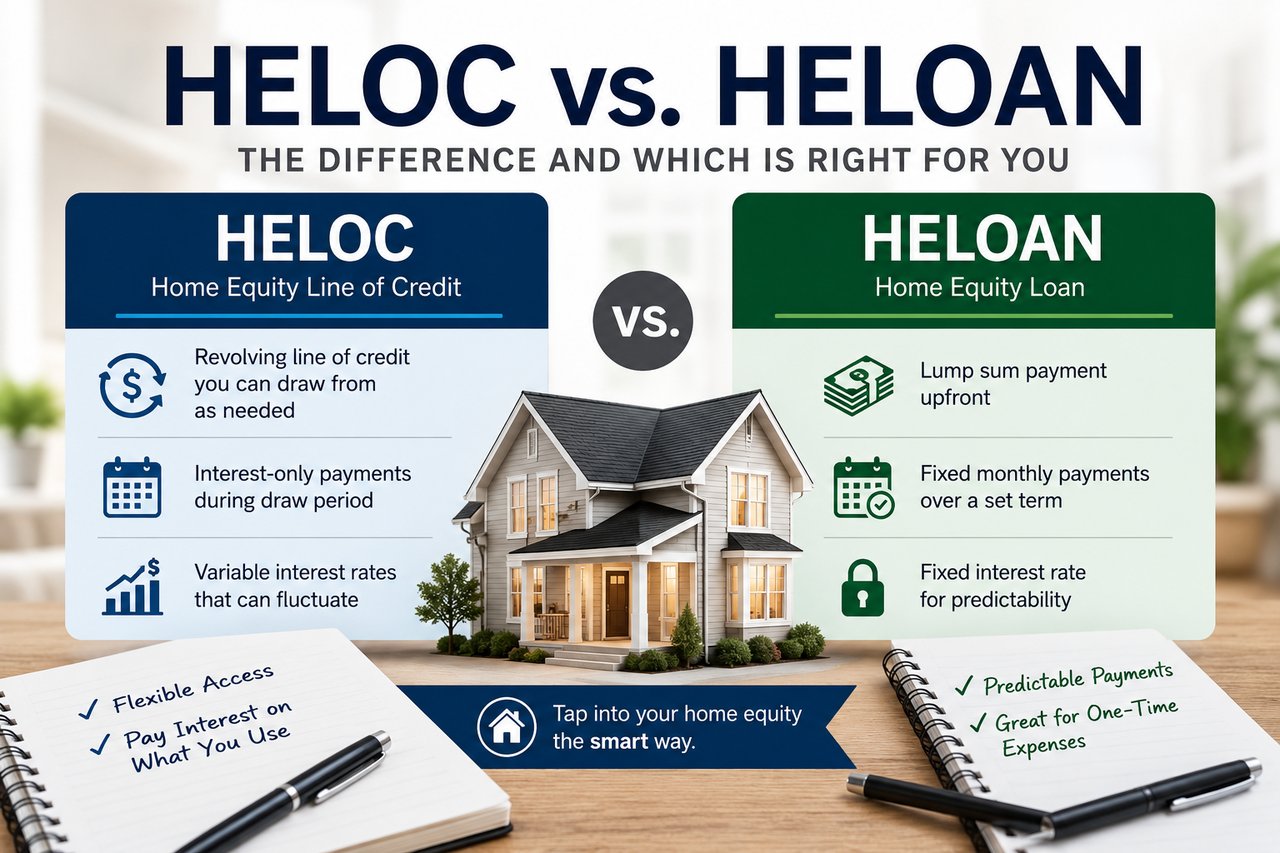

A Home Equity Line of Credit (HELOC) functions similarly to a credit line secured by your home.

Instead of receiving a lump sum upfront, you're approved for a maximum borrowing amount and can access funds as needed.

Revolving line of credit

Borrow only what you need

Interest charged only on funds used

Typically lower upfront costs

Variable interest rate

Ability to repay and re-borrow during the draw period

Let's say:

Home Value: $800,000

Current Mortgage Balance: $380,000

A lender may approve a HELOC up to approximately $300,000.

If you use $75,000 for a kitchen remodel, you're only paying interest on the $75,000 you've borrowed, not the entire credit line.

A Home Equity Loan works much more like a traditional mortgage.

You receive the entire loan amount upfront and begin making fixed monthly payments immediately.

Lump sum disbursement

Fixed interest rate

Fixed monthly payments

Predictable repayment schedule

No revolving access

Protection from future interest rate increases

Using the same home:

Home Value: $800,000

Mortgage Balance: $380,000

If you borrow $200,000 to build an ADU, you'll receive the entire amount at closing and begin repaying it immediately with a fixed payment schedule.

| Feature | HELOC | Home Equity Loan |

|---|---|---|

| Funds Available | Draw as needed | Lump sum |

| Interest Rate | Variable | Fixed |

| Monthly Payment | Can fluctuate | Predictable |

| Interest Charged On | Amount used | Full loan balance |

| Flexibility | High | Moderate |

| Rate Risk | Yes | No |

| Closing Costs | Typically lower | Typically higher |

| Best For | Ongoing projects | Defined expenses |

If you're remodeling over several years, a HELOC allows you to access funds as each phase begins rather than paying interest on the full budget from day one.

Many business owners use a HELOC as a financial buffer during slower revenue periods due to the flexibility and lower borrowing costs.

Investors often establish a HELOC before they need it, giving them fast access to down payment funds when opportunities arise.

If your contractor has submitted a firm bid and your costs are known, locking in a fixed rate can provide valuable certainty.

Replacing high-interest credit card balances with a lower fixed-rate loan can dramatically reduce interest costs and simplify monthly budgeting.

College tuition, large renovations, or significant life events often align well with the structure of a fixed-rate home equity loan.

Pay interest only on funds used

Flexible borrowing

Lower upfront costs

Potentially lower payments during draw period

Benefits if interest rates decline

Variable interest rates

Potential payment increases

Requires financial discipline

Possible payment shock when draw period ends

Fixed interest rate

Predictable monthly payment

Clear payoff timeline

No future rate exposure

Interest begins immediately on full balance

Higher closing costs

Less flexibility

Refinancing may be required if rates fall substantially

Choose a Home Equity Loan if:

You know exactly how much money you need

You want payment certainty

You're funding a defined project

You're consolidating debt

Choose a HELOC if:

Costs are uncertain

Projects will happen over time

You want ongoing access to equity

You need flexibility for investing or business purposes

Most lenders prefer a CLTV below 80% to 85%.

680+: Typically eligible

720+: Better rates

760+: Top-tier pricing

Most lenders prefer total monthly obligations below 43% to 45% of gross income.

An appraisal will typically determine your current available equity.

Neither is universally better. The right option depends on how you plan to use the funds.

Potentially. Current IRS guidelines generally require the funds to be used to buy, build, or substantially improve the home securing the loan. Consult your CPA.

Most lenders want you to maintain at least 15% to 20% equity after borrowing.

Yes. Lenders may reduce or freeze a HELOC if property values decline significantly or financial circumstances change.

The line closes and the balance converts into a repayment period where both principal and interest are due.

Over the past several years, many homeowners throughout Seattle, Bellevue, Kirkland, Redmond, Sammamish, Mercer Island, and surrounding communities have accumulated significant home equity.

The question isn't simply how much equity you have.

The more important question is:

How can that equity best support your long-term financial goals?

Whether you're considering a renovation, investment property purchase, ADU construction, debt consolidation, or another major financial decision, understanding your options is the first step.

Before speaking with a lender, it often helps to have a clear understanding of your home's value, available equity, and how a particular financing strategy may align with your real estate goals.

If you'd like to discuss your options or understand how much equity may be available in your home, I'd be happy to help.

Brian Side

Founder & Managing Broker

Upside Properties

This article is for educational purposes only and does not constitute mortgage, tax, or legal advice. Loan products, rates, and qualifications vary by lender. Consult qualified mortgage and tax professionals regarding your specific situation.

June 4, 2026

A Greater Seattle and Eastside homeowner's guide to understanding the differences, advantages, risks, and best uses for HELOCs and home equity loans in today's market.

May 13, 2026

Seattle Real Estate Market Update

April 27, 2026

And Why Right Now Is the Time to Pay Attention

Market Insights

January 26, 2026

Where the Housing Market Stands in Early 2026 and What It Means for Buyers and Sellers in Seattle

Market Insights

January 23, 2026

Rates, wages, and prices are not the real problem. Supply is.

January 15, 2026

May 27, 2025

How New Rent Control Laws Could Affect Rental Availability and Housing Affordability in Washington

May 23, 2025

Major Rent Law Changes in Washington: Limits, Notices, and Delivery Rules Explained

May 8, 2025

Understanding the Connection Between Global Trade, Local Jobs, and Housing Challenges in the Pacific Northwest

Unlock the door to your Seattle real estate dreams with Upside Properties. Experience the confidence and peace of mind that come from working with a team that puts your interests first. Contact us today to schedule a consultation with one of our knowledgeable agents and embark on an exciting journey towards finding your perfect home.

Get In Touch With Our Team To Learn More

2026 Fairview Ave E Seattle, WA 98102